The Grandparent 529 Advantage: Tax Alpha, Aid Optimization, and Generational Stewardship

The Grandparent 529 Advantage: Tax Alpha, Aid Optimization, and Generational Stewardship

As both a university professor and financial practitioner, I am often asked about the benefits of grandparents opening 529 educational savings accounts for their grandchildren. So, I thought it would be helpful to share some of the fundamentals about why this can be a powerful family stewardship strategy. For many families, education represents one of the largest financial commitments they will ever make, yet one of the most effective strategies available today to fund education costs remains often underutilized: the grandparent-owned 529 plan.

When utilized thoughtfully, a 529 plan can serve as far more than a college savings vehicle. It becomes a powerful tool for tax efficiency, estate planning, financial aid optimization, and multi-generational stewardship. So, let’s walk through some of the reasons why this strategy can empower families today, along with their future generations.

Why Grandparents Should Consider Opening a 529 Early

A 529 plan allows investments to grow tax-deferred, with tax-free withdrawals for qualified education expenses. For grandparents, this creates several distinct advantages. They can begin compounding early, reduce their taxable estate, maintain full control of the assets, and intentionally support current and future generations with education funding. Time is the greatest ally here. The earlier the account is funded, the greater the long-term impact of compounding and investment growth.

2026 Tax Advantages: State and Federal

At the federal level, contributions are not deductible. However, the growth is tax-free and qualified withdrawals remain tax-free. For South Carolina residents, where I live and work (check your state as they vary), the benefits are significantly enhanced through the Future Scholar 529 Plan. Contributions are fully deductible against South Carolina income, and qualified withdrawals are not taxed at the state level. For example, a $19,000 contribution could generate approximately $1,178 in state tax savings, assuming a 6.2% marginal tax rate. This creates an immediate and tangible return on contributions.

2026 Gifting Strategy

The annual gift exclusion for 2026 is $19,000 per person, per beneficiary. A married couple can contribute $38,000 per grandchild each year without using any lifetime exemption. For those seeking to accelerate the strategy, the five-year election rule allows for front loading contributions. Thus, a grandparent can contribute up to $95,000 at once, or $190,000 for a married couple, and elect to treat it as spread over five years for gift tax purposes. This approach allows families to move assets out of the estate immediately while maximizing the time horizon for growth.

What 529 Funds Can Be Used For Without Penalties or Taxation

529 plans are far more flexible than most realize. Funds may be used for private K-12 tuition, with a federal limit of $20,000 per year, per student. Of course, they cover undergraduate and graduate education, trade schools, apprenticeships, and a growing list of professional certification programs, provided the program qualifies. This flexibility makes the 529 a lifelong education funding tool for the entire family, not just a college savings account for one family member.

The Financial Aid Advantage

One of the most compelling benefits of a grandparent owned 529 plan lies in its treatment under financial aid formulas. Under the current FAFSA rules, parent owned 529 plans are counted as parental assets, which can reduce aid eligibility by up to 5.64% of the account value. In contrast, grandparent owned 529 plans are not counted as assets. In addition, distributions from these accounts are no longer treated as student income under the updated FAFSA rules.

The result is a potentially meaningful increase in financial aid eligibility, often amounting to thousands of dollars over time. It is important to note that some private institutions using the CSS Profile may still consider these assets so check with your specific college.

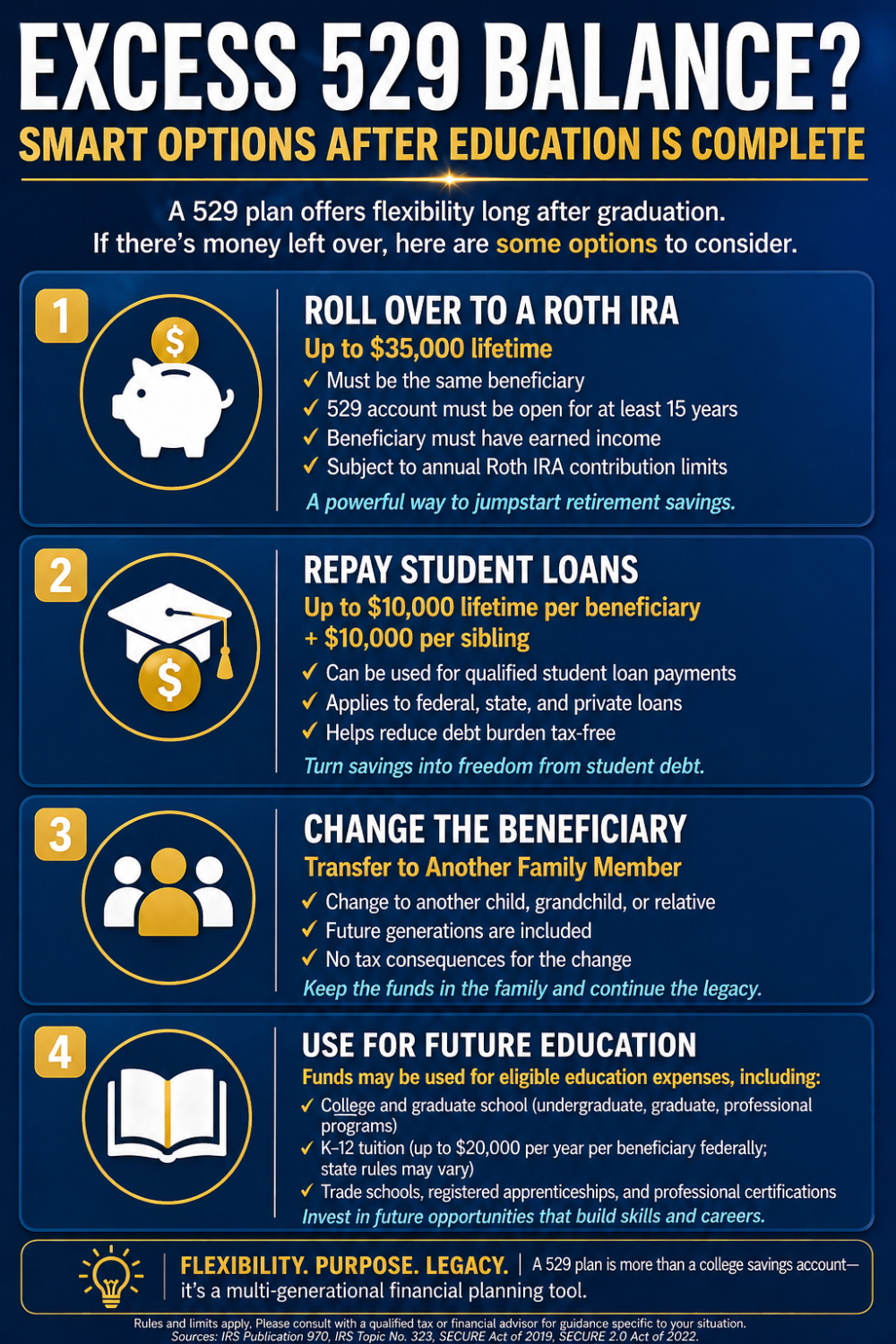

What Happens If There Are Excess Funds?

A well-structured plan anticipates flexibility. First, up to $35,000 can be rolled into a Roth IRA for the beneficiary, subject to conditions including a 15-year account history, earned income requirements, and annual contribution limits (currently $7,500 a year). Second, up to $10,000 can be used to repay student loans for the beneficiary, with an additional $10,000 available for each sibling (this could be a game changer for the family!). Third, the beneficiary can be changed to another family member, including future generations, without tax consequences. Finally, the funds can remain in place for future education, including graduate school or qualified professional certification programs.

Caution: Non-Qualified Withdrawals and Tax Impact

If funds are used for non-educational purposes, only the earnings portion is subject to tax and penalty. Consider an account valued at $100,000, with $70,000 in contributions and $30,000 in earnings. If withdrawn for non-qualified use, the $70,000 of contributions is returned tax free. The $30,000 of earnings is taxed as ordinary income and subject to a 10% penalty. For a taxpayer in the 24% federal tax bracket, this results in $7,200 of federal tax and a $3,000 penalty, for a total cost of $10,200 for a non-qualified withdrawal of $100,000 in this example.

How Much Should Grandparents Contribute to a 529?

Let’s model a practical scenario. Assume the current cost of a four-year education is $200,000. With inflation at 3% annually over 15 years, the future cost would be approximately $311,600. If the goal is to fund 75% of that cost, the target becomes approximately $233,700. There are two primary funding approaches.

- A lump sum investment today, assuming a 7% return over 15 years, would require approximately $84,700.

- Alternatively, annual contributions can be used. With a 7% return over 15 years, the future value factor is approximately 25.13. Dividing the target of $233,700 by this factor results in an annual contribution of about $9,300, or roughly $775 per month.

Takeaways To Consider

As one can see, a grandparent-owned 529 plan is not simply an educational savings vehicle, it is a comprehensive planning tool that also integrates tax efficiency, estate reduction, financial aid optimization, and legacy planning. It allows families to align financial resources with long-term purpose in a disciplined and intentional way. When structured properly, a grandparent 529 plan enables families to fund education, preserve wealth, and extend generosity across generations with greater clarity, wisdom, and efficiency. It is one of the most practical ways to turn financial resources into lasting impact as generational family stewards. So, take a closer look at the grandparent 529 advantages with your financial professional to see if it is an optimal fit for your current family and future generations.

"A good man leaveth an inheritance to his children's children..." Proverbs 13:22

For informational purposes only. Not investment, tax, or legal advice. Investing involves risk, including loss of principal. Past performance does not guarantee future results. For further information please see our full disclosure page: https://wildesfinancial.com/disclosures